Skip to content

Skip to content

Lula is unapologetically built for speed. In a landscape where bank credit can take weeks, Lula pushes decisions in minutes and pay-outs in as little as a day—backing South African SMEs with revolving working capital and short-term advances while pairing it with a modern business bank account. For SMEs that trade daily and can’t afford cash-flow stalls, that combination is a serious advantage.

Business Funding

What makes Lula compelling is the mix: on-demand capital (via a Revolving Capital Facility), fixed-term funding (via a Capital Advance), transparent fee-based pricing, early-repayment savings, and a digital application that pulls read-only bank data—no branch visits, no printing, no fuss. The end goal is simple: faster access to money, more control over repayments, and fewer hoops to jump through.

Overview

What Lula is (and isn’t).

Lula (formerly Lulalend) is a South African fintech that provides unsecured SME funding—primarily working-capital style products—alongside a business bank account delivered in partnership with a major local bank. The funding is designed for established small businesses (not brand-new startups) that can show real revenue and at least a year of trading history. Funding limits are positioned for SMEs that need quick, decisive injections of cash to stock up, bridge invoice gaps, grab discounts, or ride seasonal peaks.

What you can apply for.

- Revolving Capital Facility: An always-on line of capital you can draw down when needed, without starting a new application each time. Repay early, redraw when you qualify again.

- Capital Advance: A once-off lump sum repaid over a fixed term (3, 6, 9, or 12 months) with a clear, pre-agreed cost.

Who it’s for.

Retailers managing inventory cycles. Contractors bridging project milestones. Professional firms covering payroll while invoices clear. Hospitality operators preparing for holiday peaks. Manufacturers bulk-buying inputs to secure better margins. If cash flow is your heartbeat, Lula aims to be the defibrillator.

Features

- Funding up to R5,000,000 for qualifying businesses.

- Two core products: Revolving Capital Facility (flexible, redrawable) and Capital Advance (fixed term, fixed fee).

- Fast application: Online in minutes; share read-only bank data or upload statements; decisions typically fast and pay-outs often within 24–48 hours after acceptance.

- Unsecured: No asset security required; affordability and performance drive the decision.

- Early-repayment benefit: Settle sooner and pay less—no early-settlement penalties.

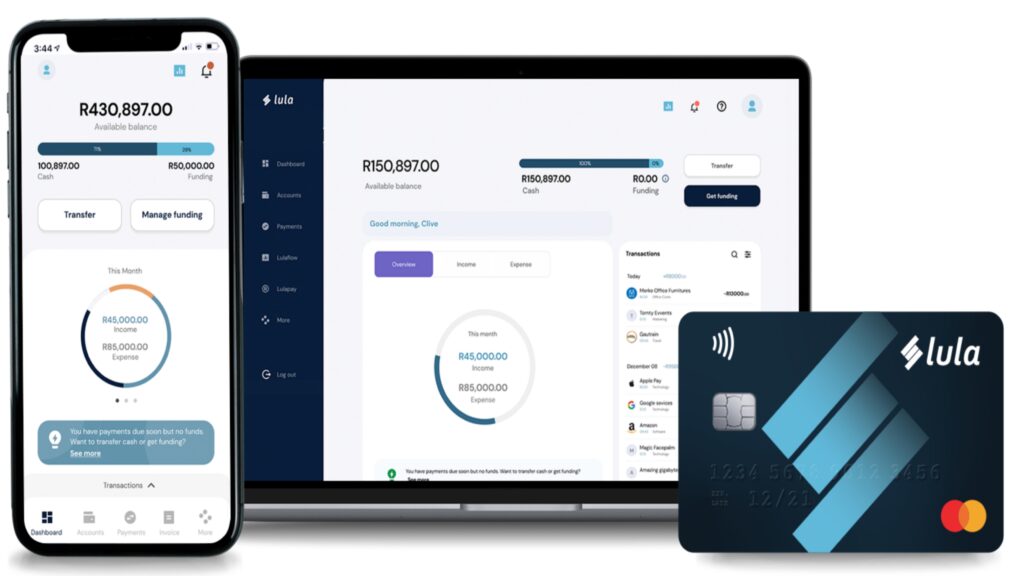

- Digital banking companion: Business account and card to manage cash flow, reconcile transactions, and keep everything in one ecosystem.

- Sector-agnostic: Widely used by retail, construction, hospitality, professional services, light manufacturing, and more.

Pricing (How costs actually work)

Lula uses a fixed-fee model on advances (rather than a compounding interest rate) and pay-for-what-you-use economics on revolving capital. That means your total cost is transparent up front—and if you repay earlier than scheduled, your cost drops because there’s no early-settlement penalty. Typical terms are 3, 6, 9, or 12 months.

Simple example (illustrative):

- Say you take a Capital Advance of R200,000 over 6 months. Your quote shows a fixed total cost and a clear monthly repayment. If you settle in month 3, costs scheduled for months 4–6 are not charged—so you save.

- With the Revolving Capital Facility, withdraw only what you need. Costs apply to the drawn amount. Repay and your available capital replenishes (subject to ongoing affordability).

Why SMEs like this model

- You can model cash flows with certainty (no surprise compounding).

- You can rotate stock or complete projects and then settle early to cut your total cost.

- You avoid the sunk time cost of reapplying every few weeks.

User Base (Who typically qualifies)

- Minimum trading history: ~12 months.

- Minimum annual turnover: ~R500,000.

- Jurisdiction: Business registered and operating in South Africa.

- Evidence: Recent bank statements or a secure, read-only bank-data link.

Good fits

- SMEs with consistent revenue and seasonal variability.

- Businesses that benefit from early-payment discounts to suppliers.

- Firms that juggle invoice cycles (e.g., 30–60 day terms) and need to cover payroll and inputs in the meantime.

Advantages

- Speed: Application in minutes; decisions and disbursements can be rapid.

- Clarity: Fixed-fee pricing and no early-settlement penalties on the advance.

- Flexibility: Revolving facility lets you draw and repay on your rhythm.

- No security: Unsecured, so no liens over machinery or vehicles.

- Banking + funding together: One ecosystem to see cash in/cash out, plan repayments, and keep discipline.

- Tech-driven approvals: Real-time business performance weighs more than just a traditional credit file.

Disadvantages

- Cost vs bank overdraft: Faster access and unsecured risk typically mean higher total cost than a secured bank facility.

- Tenor is short: 3–12 months suits working capital, not long-dated capex.

- Eligibility floor: If you’re under a year old or below R500k revenue, you’ll likely need alternatives until you grow.

- Discipline required: Flexible capital can be overused; plan draws against real cash-in dates.

Safety & Trust

- Read-only bank-data sharing: Link securely to share transactions without granting money-movement rights.

- Affordability checks: Ongoing reviews protect both your business and the lender.

- No early-repayment penalty: Encourages prudent, opportunity-driven use.

- Reputable partnerships: Card issuing and bank-account services are delivered with established, regulated partners.

- Privacy & compliance: Expect POPIA-aligned data handling and standard security controls (2FA, encryption) appropriate to fintech providers.

How to Apply (Step-by-step)

- Start online. Provide basic business details and funding need.

- Share bank data. Link your account (read-only) or upload statements (typically 3–6 months).

- Get a quote. You’ll see the amount, term options, and the all-in fixed fee.

- Accept and fund. Sign digitally; funds are paid to your nominated account—often within a business day after acceptance.

- Manage & repay. Track repayments in your dashboard. Repay early if the cash arrives sooner, then redraw later (if using the revolving facility).

Pro tips to boost approval & limits

- Keep your business account ring-fenced (don’t mix personal and business flows).

- Maintain steady balances and avoid frequent unpaid debits.

- Upload VAT and management accounts if available; richer data, better limits.

- If you run seasonal spikes, pre-apply ahead of the peak to ensure capacity when you need it.

Comparisons & Alternatives

- Retail Capital (TymeBank): Turnover-based advances settled as a % of card sales—great if POS revenue is dominant, less so for B2B.

- Merchant Capital: Similar card-turnover model; good for retail/hospitality with strong card swipes.

- Bridgement / GENFIN / Payabill: Invoice, PO, or trade-specific funding if your bottleneck is supplier credit or debtor days.

- Banks (overdraft/term loan): Cheaper when approved, but slower and often secured.

- SEFA / NEF / IDC (public DFIs): Suited to development mandates and larger/longer projects; timelines are longer and documentation deeper.

When Lula wins

- You need speed and simplicity with transparent costs.

- You value flexible redraws and no penalty for early settlement.

- You’re running a short cash-cycle business (stock-in → sell → repay).

When a bank/DFI wins

- You have hard assets to pledge and time to wait.

- You need a multi-year facility for equipment or plant.

- Your goal is the lowest possible cost and you can meet collateral/covenant demands.

Example Use-Cases (Mini Playbooks)

Retail stock-up before peak

- Draw R750k from the Revolving Facility, buy at a supplier discount, sell through December, clear the balance in February—saving fees via early settlement, then redraw for Easter.

Construction progress-payment gap

- Capital Advance over 6 months to bridge from site start to the first milestone. When the certificate pays, settle early and reduce total cost.

Professional services payroll

- 3-month term to carry payroll while enterprise clients pay on 60-day terms. Clear once the big invoice lands; repeat as needed.

FAQs

1) What funding can my business get from Lula?

A Revolving Capital Facility (flexible, redrawable) or a Capital Advance (fixed term). Limits can reach R5 million for qualifying SMEs.

2) How quickly can I get funded?

Often within 24–48 hours after you accept a quote, assuming your bank data is linked and all checks are complete.

3) What are the eligibility basics?

Typically ≥12 months trading, ≥R500k annual turnover, and a South African-registered business with active operations.

4) Do I need collateral?

No—funding is unsecured. Affordability, cash flow, and trading performance matter most.

5) Is this interest or a fee?

Advances use a fixed-fee model (not compounding interest). The revolving line is pay-for-what-you-use. Repaying early reduces your total cost.

6) What terms can I choose?

Commonly 3, 6, 9, or 12 months. Pick shorter for quick rotations, longer to smooth repayments.

7) Can I repay early?

Yes, and there are no early-settlement penalties—so you save when you settle ahead of schedule.

8) How are repayments structured?

For fixed advances, you’ll see a clear monthly amount that includes the principal portion plus the agreed fee. With the revolving facility, costs apply to the amount you draw.

9) What if my business is seasonal?

That’s the sweet spot. Use the line to ramp up, then clear in the off-season. Early settlement cuts cost.

10) What documents are needed?

Basic business info and recent bank statements (or a secure read-only link). Financials can help increase your limit.

11) What if I’m a sole proprietor?

You can still apply if the business meets the time-in-business and turnover thresholds.

12) Will frequent draws hurt my chances later?

Not if you manage them well. Consistent on-time repayments and stable cash flows can improve future offers.

13) What’s the difference between Lula and a bank overdraft?

Speed and security: Lula is faster and unsecured, with transparent fees; an overdraft can be cheaper but usually needs collateral and more documentation.

14) Can I use Lula for equipment?

It’s primarily working capital. For heavy capex, compare with bank asset finance or DFI options—but a short-term advance can still bridge deposits.

15) Does Lula offer a business bank account?

Yes—Lula pairs funding with a digital business account and card, helping you centralise cash-flow management and payments.

Final Verdict

If your biggest constraint is time to cash, Lula is built for you. It blends speed, clarity, and flexibility: fast decisions, transparent fixed fees, no early-settlement penalties, and a revolving line that moves with your business. Add the companion banking features and you get a simple, modern stack that helps SMEs buy earlier, sell faster, and pay less when they settle early. For working-capital problems that can’t wait, Lula is a strong, pragmatic choice—and one worth short-listing on any South African SME’s funding page because Lula turns “we need cash today” into “we can do this tomorrow.”